Where N = Number of Segments

S = The percentage share of the ith segment

The European Automotive Industry

SEGMENTATION AND STRATEGIC GROUPS

In this section we shall discuss segmentation and strategic

groups. These two are interre-lated, as we use the market

segmentation to divide the actors into strategic groups.

While segmentation analysis concentrates on the characteristics

of product markets as the basis for dividing industries,

strategic group analysis uses the characteristics of firms as the

basis for division. When the nature of intensity of competition

varies within an indu-stry, it is useful to divide the industry

into segments and analyse its structural characteri-stics.

Segmentation is not only useful for the new entrants in

determining which part of a market to enter, but also for the

established firms in deciding in which segments to main-tain a

presence and how to allocate resources between them .

Strategic groups are defined as clusters of firms within an

industry that have common characteristics and thus follow the

same or similar strategies in setting key decision varia-bles.

These key decision variables may include product market scope,

choice of distributi-on channels, levels of product quality,

degree of vertical integration, choice of technology and so on. A

strategic group is part of an industry that may play a role in

understanding performance differences among firms. One group of

firms may exhibit high advertising to sales ratios, extensive

marketing efforts, careful attention to services and wide brand

ran-ges. Other groups of firms in the same industry may follow

the quite different strategy, focusing perhaps on volume

production of a single brand.

In terms of analysis, the strategic group is a middle ground

between the industry and the firm. In some industries, the group

structure is obvious and very important. In other indu-stries,

some differences in strategies among firms seem to exist, but

they only play a little permanent role in the evolution of the

industry. Strategic group analysis is unlikely to of-fer much

insight into why some firms are more profitable than others. It,

however, provi-des a broad picture of types of firms within an

industry. Furthermore, It can contribute to an understanding of

the structure, competitive dynamics and the evolution of an

industry and to issues of strategic management within it.

MARKET SEGMENTATION

The European market for passenger cars consists of a number of

different sized automo-biles. In this section we will discuss the

segmentation of the European passenger car mar-ket.

There are numerous ways in which the car market can be segmented,

but it is usual to divide it into some distinct groups according

to a combination of size and price. The UK motor industry trade

association, the society of Motor Manufacturers and Traders

(SMMT), has now formalised segmentation into nine market segments

on the basis of vehicle size, and this method has been widely

accepted throughout the industry.

Nine segments have been identified, and together they cover

almost 99% of the European car market. Each is defined as follows

:

# A segment-mini

# B segment-small

# C segment-lower-medium

# D segment-upper-medium

# E segment-executive

# F segment-luxury

# G segment-sports

# H segment-dual-purpose

# I segment-multi-purpose vehicle (MPV)

In this project, we will mainly analyse the first 7 segments (A -

G), as the H and I seg-ments are less well defined, and make up a

small part of the total market.

Segmentation Overview

Before we discuss the details of each segment, we will present a

quick overview of the markets overall segmentation.

Indsæt figure 6.1 fra side 76

Two segments, small cars and lower-medium cars, both of which

account for a 30% mar-ket share, dominate the European market.

The upper-medium sector is slightly smaller than the other two

sectors, but if one add these three together, it accounts for

over 80% of the total market in terms of units.

The other segment with a significant volume of vehicles is the

executive car segment, while all others are considered to be

niche markets.

The concentration of the market within these three main sectors

influences the strategy of the manufacturers. Companies such as

Mercedes-Benz and Audi have had very little inte-rest in these

segments historically, but because of the big market share of

these three seg-ments, they can't ignore them, and are now

introducing or planning models in these seg-ments in order to get

a bigger market share. On the other hand, the companies, which

tra-ditionally dominated these segments, are now looking at ways

of breaking down each market area into sub segments and offering

specific models for each. An example of this is the C segment,

which we shall discuss later in section 6.1.4.

The smaller market segments are also important to most

manufacturers. Such smaller and niche market segments often

represent new or growing markets that are important for all

manufacturers.

In appendix C we have produced a table, showing the importance of

different segments in different markets. Further in Appendix D,

we have shown the importance of different segments to different

manufacturers.

6.1.2 Segment A: Mini Cars

This segment has never been a major part of the overall car

market in Europe, and demand for these vehicles fluctuate

significantly. In the European market, the consumers tend to

think that these cars are too small for general use.

Although the cars are priced at the entry level for the car

market, most new car buyers bypass this segment and move straight

to the B segment. Consequently the A segment has not grown in

recent years.

Italy is by far the largest market for mini cars, with more than

twice as many registrations as France. Generally speaking mini

cars are more popular in southern Europe, except for Spain and

Portugal that have below average shares of their markets

controlled by minis. The use of mini cars in Scandinavia is

almost non-existent.

Most of the broad line manufacturers now produce so called sub-B

segment cars, which are cut-down versions of B segment cars

rather than specific designs for the A segment. In this segment,

Fiat Cinquecento and the Renault Twingo have been very

successful. Ford launched the Ka in the late 1996 and GM will

follow with a more conventional sub-B model in 1997. Volkswagen

launched SEAT Arosa and Lupo in early 1997. Mercedes-Benz in a

joint venture with SMH of Switzerland will launch the Smart Car

in 1998. The pure A segment seems to be fairly static in terms of

growth, but there could be a lot of potential in the sub-B class.

However, at present Fiat totally dominates this segment, with 78

% of the market .

Segment B: Small Cars

The B segment is one of the largest two segments of the car

market. (The other one is the C segment). If all the new sub-B

cars were included in this segment, it would become larger than

the C segment.

Between 1995 and 1996, the B segment grew marginally more than

the total market and it remains the key market sector, since this

segment is the entry-level for most first-time buyers in the new

car market. In this segment, the design is usually a hatchback in

order to maximise the volume of the car with the comparatively

short length. Besides this most models provide a degree of choice

for the customer, such as the choice of 3- or 5- doors and a

variety of engines, including diesel.

Among the models in this segment, the Fiat Punto is the best

selling car . In 1996, the new Fiesta and the Corsa sales

increased too. The Polo also rose sharply, whereas the Clio,

which was the segment leader in 1992, dropped away further.

Typically, the best-selling model will sell about 600,000 cars,

but it is a very competitive sector and the lea-der changes

frequently. In recent years Fiat, Ford and Renault have led the

sector, becau-se of the high volumes involved.

The B segment is likely to grow in the future as a function of

the ageing population, a growing car parc and changes in

household structures, such as the growth in single house-holds

and retired lifestyles. Linked with this, is the increase in

individual choice with the rise of multi-car households.

The B segment has been fragmented into four broad groupings. The

advantage of doing this is that manufacturers can reorganise the

product line-up in order to target an increa-singly fragmented

market. Thus the 90's has seen the emergence of three sections

within the B segments. There are the traditional cars, which are

practical general purpose cars, and small cars designed for urban

driving, as well as new cars with improved driving dy-namics.

Further, some of the high-end producers have introduced small

luxury cars in this segment.

The market share for this segment in the European Market as a

whole, is 30%, but in France and Italy it is well over 40% and in

Portugal over 50%. In the Scandinavian coun-tries the market

share is rather small, as well as in the German Market.

Segment C: Lower Medium

This segment is the largest segment of the European car market

and the most competitive one too.

It is the area where private buyers of new cars and company

buyers overlap. Competition is further increased in this segment

because both traditional manufacturers of small cars, and

up-scale manufacturers eye this market. The sector grew by 7.3%

in 1996, which is 1 %-point more than the market average.

VW is the largest company in this segment, due to its highly

successful Golf model . The other leading models are Opel Astra

and Ford Escort. Although the sales of these three models are on

decline, they still hold on to their leading position. Several

up-scale manufacturers have entered this segment in 1996, such as

Audi A3 and the Mercedes-Benz A-class. This is a logical move for

both companies as they are extending their range into a large

market where they have not previously been represented.

The market share for this segment is relatively even across

Europe. The big markets such as Germany, France and the UK are

fairly near the average. Italy is relatively small be-cause it is

so much stronger in small cars. Denmark, Austria, Finland and

Ireland are large markets for this segment.

Segment D: Upper Medium

Segment D is the 3rd largest segment after B and C segment as it

accounts for 21% of the market. It grew by 7% in 1996, more than

the market as a whole, but no company domi-nates this sector.

In the late 1980s and early 1990s GM's Opel Vectra was the best

selling car in this seg-ment. Ford fought back with the Mondeo,

and achieved leadership from 1993. By 1995 there were six models

outselling the GM Vectra/Cavalier, however in 1996 the full power

of the GM marketing effort was brought to bear, and the Vectra

once again became the top-selling car. All its competitors

slipped back in 1996 with the exception of the Audi A4 and the VW

Passat.

This segment is popular throughout Europe, although it is

stronger in northern Europe than it is in south. Of the four

largest markets, Germany and UK are strong, while France and

Italy are relatively small in the D segment. Conversely in

Belgium, Netherlands and all the Scandinavian countries, D

segment cars are popular. In Denmark, Finland and Norway it holds

over one-third of the market shares.

Segment E: Executive cars

The executive car segment is a relatively small part of the

European market, with less than 10% of the total. In 1996 it only

grew by 1.6%, far less than the market as a whole. The overall

share fell to 8.4%. However, it still accounts for over 1m cars

each year and it is important for the prestige of the

manufacturers involved. Thus performance in this seg-ment may

affect performance in the other segments.

Mercedes-Benz is the dominant player, with almost 40% of the

total market segment. BMW and Volvo are the other significant

manufacturers. VW does not make vehicles in this category,

leaving the field to Audi. Ford and GM participate in this

segment too. GM has share of this market with Omega model, and

Ford with its Scorpio, but in general, they are regarded as minor

players.

Germany is by far the most important market in this segment. It

accounts for over 45% of the market demand. The highest market

share is demonstrated in Sweden. The Volvo and Saab models make

the market share of E-segment cars over one-third of the market.

Fin-land, Norway, Switzerland, Luxembourg and Belgium also have

high proportion of the E-segment cars.

Segment F: Luxury Cars

This is the smallest of all segments in the European car market,

accounting for less than 100,000 vehicles. However, it is a very

prestigious and profitable segment and thus it is highly

important to the manufacturers.

The market leader in this segment is Mercedes-Benz. The largest

market by far is Ger-many, accounting for over half of all luxury

cars sold. The UK is also a substantial mar-ket, while France and

Italy are relatively small. Belgium Switzerland and Luxembourg

are significant markets for this segment, relative to their small

size.

The Mercedes-Benz has decided that they will reduce the size of

its current S-class and will introduce a larger, more luxurious

new class above the existing range. All the other manufactures in

this segment are looking into other markets. Audi, BMW and

Mercedes-Benz are all bringing out smaller cars and Jaguar is

moving back into areas of the sports segment that it had

abandoned previously.

Segment G: Specialist sports cars

This segment is a small niche in European Market, but lately it

has received much attenti-on from companies that had previously

abandoned the segment.

GM leads the market with over a quarter of all sales with its

Tigra model. Ford and GM have developed sports cars from time to

time to complement their standard range. The Opel Calibra, first

into market in 1990, sold over 60,000 units across Europe within

two years. In this section, the design of the cars is very

important and attracted to more and more customers' attention.

Therefore nearly all the big companies are have product in these

segments.

The biggest market for sports cars is Germany, followed by UK and

Italy. The market with highest penetration of sports cars is

Switzerland, closely followed by Luxembourg. Other countries with

an above average preference for these cars are Italy, UK, and

Ger-many. In contrast, the Scandinavian countries have very few

sports cars relative to their overall markets and France is below

the average.

The long-term growth of this segment is secure due to changes in

the lifestyle and an in-crease in discretionary income.

Manufacturers have invested heavily in this segment, and some new

models have and will come to the market.

STRATEGIC GROUPS

Below we shall divide the actors into strategic groups. As

mentioned above, this can be done through a number of criteria.

We shall use the segments discussed above for our strategic group

analysis.

For the first criteria we shall use diversification of product

lines. Thus the actors will be segmented on a basis of niche

players versus broad line producers. The second criteria will be

up scale versus down scale producer. For both criteria we shall

use the market segments above. Thus by diversification we mean

how well the company's products are dispersed across the

segments, while the latter criteria refers to the companys most

im-portant segment.

Finding a good measure of the latter criteria is easy. Here we

simply choose the segment in which the company sells most units.

Thus companies will be placed on a scale from segment A to G. It

would be more optimal to use sales in each segment, for this

analysis, but unfortunately such data has been unavailable. Hence

there is a bias towards the lower priced segments.

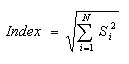

Finding a measure for the diversification criteria is more

difficult. Simply using the num-ber of segments in which the

company is represented is inadequate, since it only measures the

number of segments, and doesn't take the importance of each

segment into account. An example is Mercedes-Benz that is

represented in 3 segments, but has 91,6% of its sa-les in the E

segment. Instead we need a measure that takes the amount of sales

in each segment into account. For this we shall use the following

formula:

Where N = Number of Segments

S = The percentage share of the ith segment

This index works by squaring the market shares individually,

while the square root is ta-ken of the total. Thus firms that

operate in only one segment (Niche Players) will receive an index

score of 100, while firms that are differentiated across an

indefinite number of segments, will receive a score of 1.

The summation part of the index is the same as the

Herfindahl-Hirschman index, which is normally used to calculate

the concentration within an industry. Thus this index is simply a

different use of the HHI, although we have added the square root.

This is done to avoid the exponential character of the HHI.

In appendix D we have shown how the new registrations of

different manufactures are distributed across the segments. We

have used this to set up the table below.

Table 6.1

Source: Appendix D

The data in the table is then used to set up the diagram

below. From the diagram we can identify 4 strategic groups:

Nr. 1: Diversified Low End Producers:

Nissan, PSA, Fiat, Ford, GM, Renault Suzuki

Nr.2: Diversified High End Producers:

BMW, Mazda, Toyota and Volkswagen

Nr.3: Specialised Medium Producers:

Honda

Nr.4: Specialised High End Producers:

Mercedes, Volvo

Obviously this result is heavily dependent on the chosen

criteria. In many textbooks regarding the automotive industry, a

similar analysis is conducted with respect to the

differentiation, and the extend to which the company has a global

focus. We have chosen a different approach because this report is

focused only on the European market. Thus the global scope of

companies is of lesser importance.

The Strategic Groups below consist of companies that continuously

run into each as op-ponents in the European market. This happens

because companies in the same strategic group, focus on the same

primary segment, and run into each other across many of these

segments. For example are Volkswagen and BMW likely to compete in

almost all their market segments.

Indsæt figure 6.2 fra side 85

One should be very careful when using a strategic group

analysis in the car industry. The industry is highly competitive

in nature, and even companies that are distanced from each other

in the diagram below, are likely to compete in some market

segments. An example of this is Fiat and Mercedes, which are

positioned at opposite ends of the diagram. Even so they face

each other in the E segment (See appendix D). This demonstrates

that in the car industry, all companies compete against each

other in some ways. Thus the strategic group analysis is merely a

measure, of which companies face each other most often.

It is evident from the figure above, that there are very few

specialised manufacturers. This is an effect of the horizontal

integration in the industry. An example is the BMW group, which

use its BMW brand for vehicles at the high end of the market, and

its Rover brand for vehicles at the lower end of the market.

Another reason is that this analysis only con-tains large

companies, and thus smaller specialised companies are not

included.

SECTION SUMMARY

In this chapter we have divided the market for passenger cars in

Europe into seven seg-ments according to vehicle size. The most

important of these, are the segments for small cars and lower

medium sized cars. However luxury cars are also important for

prestige reasons, while some of the small segments are important,

as high growth is expected in these segments.

The segments have been used for an analysis of strategic groups.

Here we use diversifica-tion across segments, and primary

segments as criteria. For the first criteria we used the index in

section 6.2 to make a quantifiable measure.

Through the analysis we identified four different strategic

groups. The significance of this analysis is that firms within

each strategic group compete against each other in several

segments. Thus actors should be especially aware of the moves of

actors within their own strategic group. However, in the car

industry there is also heavy competition across these segments.