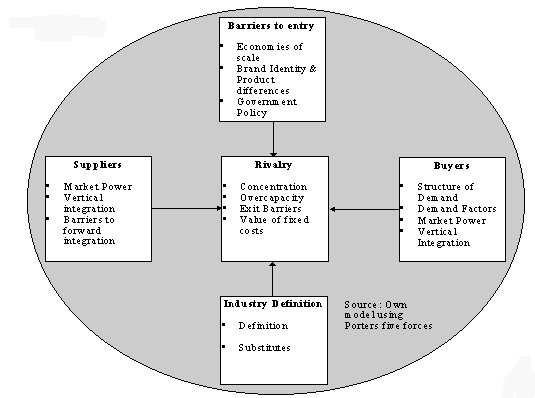

The European Automotive Industry

Industry Features

In this chapter we will

describe the basic features of the industry, and discuss how they

affect the level of competition and conduct of market actors.

As mentioned in section 2.4 we will use a modified version of

Porters five forces to describe the basic features of the

industry. The model is modified in order to concentrate on the

factors that have special relevance for the automotive industry.

Thus we will not discuss all the factors that are normally

synonymous with Porters five forces, but rather select the

factors that have special relevance and incorporate them into

Porters framework.

Figure 3.1

It should be mentioned that

this model has little analytical value in itself, and is merely a

tool for structuring the presentation of the industry. Thus, in

some cases we shall need other theories to examine the individual

features. In these cases we will state the theories used, in the

relevant section. For an overview of theories used, see section

2.4 on methodology.

As it is shown in the model we will not discuss substitutes as

intended in Porters original model. The reason for this is that

the substitutes available for private motoring have little effect

on the nature and level of competition in the car industry.

However if large monopoly power were to emerge in the industry,

public transportation as a substitute may set limits on the

prices of a monopoly producer. However, substitutes are needed in

order to define the industry. Hence we have changed substitutes

to industry definition. Of course this will be the first issue to

be discussed below.

The features relating to barriers of entry will not only be

discussed from the perspective of keeping out potential entrants,

but also from the perspective of how these factors affect actors

that are already in the industry. Under buyers we shall mainly

focus on demand, both with respect to current quantity and with

respect to the factors that influence the size of demand. This

section will contain a large amount of empirical data regarding

the size of the industry. Further we will discuss market power

and vertical integration on the supply side as well as on the

demand side. For the section of rivalry we will measure and

examine the effects of concentration. Also we shall discuss

overcapacity in the industry, as well as exit barriers and fixed

costs.

Below industry definition, rivalry, buyers, suppliers and

barriers to entry are discussed in that order. This order is not

coincidental. There is an amount of interrelatedness between the

individual factors of the model, and the order has been chosen in

an attempt to describe the most basic structures first, and their

dependants later. However, in some cases it may be necessary to

refer to a later sections.

INDUSTRY DEFINITION

Below we shall briefly define the industry in question. In order

to do so, we need to discuss not only the industry itself, but

also the possible substitutes. An industry is merely a group of

companies that produce a product with similar distinctive

features. Thus we need to identify these features.

As mentioned in section 2.5 on limitation, this report focuses on

the passenger car industry in Europe. The benefits provided to

consumers of the industry products are easy transportation, and

thus possible substitutes are other forms of transportation. In

Western Europe the main substitute for cars is public

transportation and non-motorised transportation like bicycles.

Public transportation functions as a substitute for longer

distances, whereas non-motorised transportation is a substitute

on shorter distances.

The effect of the presence of substitutes depends on the

closeness of these substitutes . That is how much they resemble

the product in question. One of the main features for personal

motorised vehicles relative to public transportation is

convenience and flexibility. However these differences are

decreasing, as public transportation is experiencing considerable

growth as an effect of pollution pressures toward collective,

low-emission forms of transportation. This has induced policy

makers to set up more advanced schemes of public transportation,

which allows for increased flexibility through more departures.

Thus public transportation is an increasingly significant

substitute to private car ownership at lower prices. This induces

car manufacturers to produce cars that are more economic with

respect to variable costs like fuel.

From the discussion above we have limited our focus to personal

motorised transportation. However, even in this category there is

a large amount of different companies, like component producers,

car dealerships etc. This report will focus on companies that

assemble the finished vehicle. All of these companies are also in

the business of making engines, and designing vehicles. However

this definition excludes companies that only produce car

components, whereas assembling companies that are vertically

integrated into component production are included.

Rivalry

Below we shall discuss some factors that affect the rivalry, and

thus the fierceness of competition in the car industry.

Concentration

Economic theory suggests that the vigour of competition is

related positively to the number of firms in the relevant

industry when other conditions such as height of barriers are

equal. There are a number of reasons for this phenomenon.

One is that in highly concentrated industries, firms have a

larger degree of market power. This is most obvious in the case

of maximum concentration namely monopoly, but market power also

occurs where there is more than one actor in a concentrated

industry. It has been estimated that in an industry where the 4

largest firms control more than 40% of the market, oligopolistic

competition is likely to occur .

The effect of such market power is that firms face a less elastic

demand curve. Thus in order to sell one extra unit, the firm

needs to reduce the price on all units, placing marginal revenue

below the demand curve. As the firm produces at MC equals MR,

price is higher than average costs. Thus there are monopoly rents

for the firm. This is shown below in figure 3.2.

In a situation where industry concentration is at a minimum,

substitution between firms will lead to a situation, where the

individual firm faces highly elastic demand. This happens because

firms cannot sell at a price significantly above the price of its

competitors, and consequently competition will push prices

towards the level of average costs. Accordingly economic rents

are minimised.

Indsæt figure 3.2 fra side 19

Indsæt billede fra s. 23

In all circumstances the

existence of overcapacity is a powerful catalyst for fierce

competition. In such an environment the marginal cost of

producing an extra unit is relatively low, and the break-even

level in terms of units sold is relatively high. Thus the firms

in the industry have a strong incentive to cut prices, in order

to stimulate demand, and consequently putting their excess

capacity to use.

Exit barriers and value of fixed costs

Another determinant of competition in the car industry is exit

barriers and the value of fixed costs. These are somewhat

interrelated since fixed costs relating to specialised assets is

an exit barrier.

The effect of high exit barriers is that firms tend to stay in

the industry, even if it is not profitable. This leads to

increased competition, as some market actors are willing to

operate at a loss in order to avoid the high costs of exit. Such

exit barriers can stem from a number of factors, like for example

contracts that are expensive to break or specialised assets as

mentioned above.

In the car industry there are a number of highly specialised

assets like production plants and the value of knowledge in the

form of R&D (R&D is quantified in chapter 7). Such assets

cannot be transferred to other industries without loosing value.

Thus if a firm chooses to leave the industry, it will loose the

value of its specialised assets. This is not the same as to say

that existing firms should always stay in the car industry. If

the firm is running at a loss, and there is no chance of turning

this situation, it will be better to incur the cost of loosing

its assets right away. However if the deficit is perceived to be

temporary, the value of assets will incite the company to stay in

the industry, in the expectation of future profits.

In the car industry, where there are a number of large producers

(see appendix A), industry specific assets are likely to be

traded among industry actors at a reasonable price. Thus there

doesn't seem to be much of a case for the high exit barriers

argument in the car industry.

High fixed costs are another catalyst for competition. High fixed

costs often lead to low variable costs and marginal costs. Thus

firms are induced to cut costs, in order to sell more, so as to

cover their high proportion of fixed costs. Fixed costs will be

further examined and quantified in chapter 7. Here we show, that

the amount of capital to labour is relatively high in the

industry, but at the same time labour costs, far exceed

depreciations. Thus although fixed costs are high there appear to

be no extreme threat for price wars. Both fixed costs and exit

barriers are related to the game theory example above, since sunk

costs are necessary to make a credible commitment to the

industry.

Industry growth

In a situation where the size of an industry is declining, there

is a struggle, to be an industry survivor. Hence low growth leads

to intense competition, whereas high growth diverts the attention

of companies towards capturing the shares of the new market, so

that competition is less head-on.

After almost fifty years of steady post-war growth, only

interrupted by the oil crises in 1973 and the early eighties, car

demand suddenly dropped by a massive 16.8% in 1993. Only 11.3

million cars were sold in 1993. This is nearly 2.1 million units

less than the previous year. In other words a loss of 2,5 billion

ECU, which is equivalent to the total output of all Western

European Volkswagen plants. The development is shown in figure

3.3 below.

Indsæt figur 3.3 fra side 25

With the benefit of hindsight, the 1993 trend

line break should not have been as unpredictable as it looked at

the time. In reality demand had started to loose its edge already

a few years earlier. However at that time the change in growth

was concealed by two extraordinary events that temporarily

boosted demand.

In 1991, after the reunification of Germany, West- European

registrations enjoyed an almost overnight windfall of an

additional 700,000 East-German registrations. Together with the

beneficial effects on West-German new car sales, triggered off by

a massive export of second hand cars to former East- Germany.

Secondly, during the years that preceded their EC membership and

during the first years of membership Southern European market

like Spain, Greece and Portugal experienced a strong increase in

passenger car sales. During the period 1984- 1989 the Spanish car

market tripled from 500.000 in 1994 to 1.5 million in 1989.

Demand eased down again to previous levels after the average age

of car parc had settled at a lower level, more in line with the

newly found wealth and increases in GDP per head.

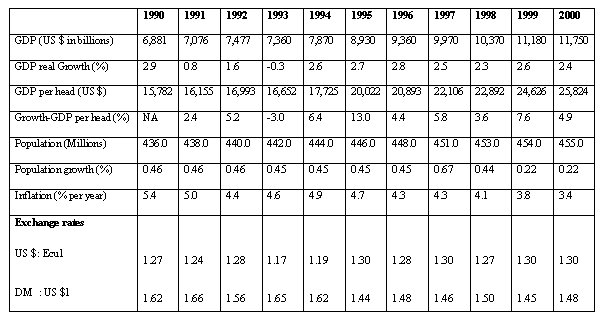

As it is shown in section 3.3.2 demand is correlated to economic

prosperity. In the table below we have shown some economic

indicators for EU15.

Table 3.1

Source: Neil Mulliniuex: The new car

market in Europe & OECD Economic Outlook.

Figures after 1996 are projected.

GDP per head has been increasing by a considerable percentage. However, GDP per head figures can be misleading because these figures do not consider differences in the cost of living, so it does not show the real standard of living. We therefore use the real GDP growth to measure economic growth, which includes differences in the cost of living. In 1994, for example, real GDP growth was only 2,6%, but growth of GDP per head was 6,4%. Real growth of GDP continued to improve in 1994 and 1995 after a period of low growth between 1991 and 1993. The economy of the region was estimated to have grown by 2,6% - 2,7% in each year. Though the European economy had below average rate of world trade growth, it was a good performance from such mature economies.

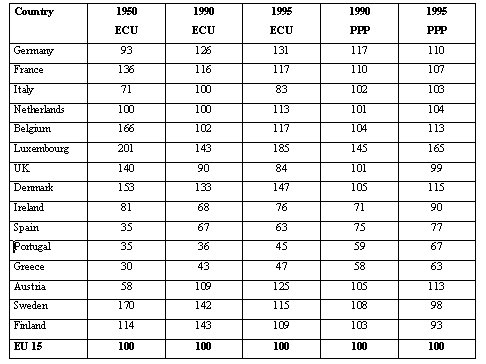

Table 3.2

Source: Molle, Willem: The Economics of

European Integration; page 439

PPP = Purchasing Power Parity

If we look at the European economy, the average

for the countries that now make up the EU15 was almost three per

cent a year over the last forty years. First there was a long

period of high and stable growth (four per cent a year) that

lasted up to the first oil crisis. This coincided with the first

extension of EU. Next there was a period of adjustments, with low

growth (1,5 percent a year). The end of this period coincided

with the second extension. Finally the period since 1985 is one

of new dynamism (growth rate of 2.5 per cent a year).

If we need to account for the differences in the cost of living,

we can use Purchasing Power Parity (PPP) index. This index allows

for more direct comparison of living standards in different

countries. In the above table PPP is set equal to 100 for the

average purchasing power in EU member countries. According to

table 3.8, Luxembourg had the highest standard of living, PPP

165, in1995, while Greece had the lowest standard of living, PPP

63, in EU. It means that an average citizen of Luxembourg's

purchasing power was nearly three times higher than an average

citizen of Greece.

All in all projected growth in Europe is moderate. Certainly the

potential for growth is not as big, as it tends to be projected

in the annual reports of the manufacturers. Combined with

saturated markets it does not appear that demand for cars is

likely to increase significantly in Europe. This low growth

environment is likely to increase competition in the industry.

However there may be a possibility for high growth in the East

European countries, if some of these are accepted for an EU

membership. Acceptance may lead to rapid Economic growth in these

areas, and hence a temporary boost in car demand, like the one in

Southern Europe in the late 80's.

BUYERS

Below we shall discuss the elements in the buyer section. These

include vertical integration, market power and demand. Demand has

been subdivided into three sections. The first, structure of

demand, presents empirical data on the sales of automotive

vehicles in different countries. The second section discusses the

factors that drive demand, while the third section discusses the

effect of segmented markets.

Structure of Demand

The table below shows the unit sales of passenger cars in 17

European countries in the period from 1991 to 1996.

Figure 3.3

Source: Neil Mullinieux: The new car

market in Europe; page 5

According to the table, the European total

market grew by 6,3% in 1996 and the growing convergence of the

European economies resulted in all countries showing positive

growth over the previous year. However, it is clear that all the

markets are mature to a greater or lesser degree. Only the

Norwegian car market is growing strongly. In other words, it

seems to be recovering to original levels from a deep depression.

There is still some overall growth potential in the southern

markets of Portugal, Spain and Greece, but even here the sale of

passenger cars is influenced far more by the immediate health of

the economy than by longer-term growth in GDP.

The five largest countries, namely Germany, France, Italy, UK and

Spain, dominate the European demand for automotive vehicles,

which is demonstrated in figure 3.4 below. Together these

countries accounted for 80,4% of car sales in 1996.

Indsæt figure 3.4 fra side 30

Despite a fall in sales from 4,158,674 units in

1991 to 3,496,320 units in 1996, Germany remained in a dominant

position in the market, accounting for 27.4% of all sales. The

German car market was already the largest in Europe before

unification and it has now risen to a new level. It is the key

market for any manufacturer, not just because of its size, but

because it consists of larger and more expensive vehicles than

most other countries .

France, Italy and the UK are markets of almost the same size,

with annual demand of nearly 2 million vehicles in each market,

each having approximately 15% of the European total market share.

While the UK, Spanish and French car markets recovered in 1994,

the demand for new cars declined further in Germany and Italy.

Recovery in French and Spanish market was boosted by

government-sponsored incentives for car replacement. Over the

last two years several governments have adopted the French idea

of offering incentives to stimulate the sales of passenger cars.

Usually this has taken the form of direct reduction in the price

of a new car, if cars of certain age were being replaced. The

stated rationale for this type of incentive was usually

environmental .

In Western Europe car ownership is about 20% below the level in

the USA, although the key markets of Germany, Italy and France

are much nearer to the American average . There are some other

factors, which will prevent car ownership in Europe ever reaching

the level in the USA. Europe has a smaller land area and a larger

population compared to USA. The average population density is

higher and this inhibits car ownership, particularly as more

people live in cities. By their very nature cities discourage the

use of cars by making it difficult to park, while they have

enough public transport services. Further more, most European

cities are much older than cities in the USA. Therefore it is not

easy for European cities to fulfil the special requirements of

wide and straight roads and plenty of parking space.

The European passenger car market, however, is large in

production and in turn over. It contributes nearly 1/3 of the

global car market. Worldwide sales of new cars increased from

33,1 million units in 1993 to about 35,0 million in 1994. At the

same time in the EU market, sales recovered to 11,2 million units

in 1994 from 10,7 million units in 1993. In 1996 sales of new car

in the European market increased to 12,8 million from 12,0

million in 1995. Even though this 6,3% of growth in the market

was extraordinary, the manufacturers did not seem to be well and

many of them experienced considerable problems in terms of low

margins and high marketing expenses . This is an indication of

tough competition.

Demand Factors

In the following pages we will aim to identify the factors drive

demand, and examine them. Where empirical data on a suggested

factor is available, we shall also seek to demonstrate the

relationship to demand.

Table 3.4

Source: Neil Mullinieux: The New Car

Market in Europe; Page 230

In order to do so, it is necessary

to begin with a few definitions relating to the size of demand.

The vehicle parc is the number of vehicles in use within a

market. Approximately 75 percent of the world's vehicle parc are

within developed markets, and it is set to exceed one billion

vehicles in 2015, of which just 59 percent will be in developed

markets. Vehicle parc change slowly, as parc dynamics revolve

around a current average vehicle life of 6-7 years and overall

parc renewal every 13 to 14 years. The rate of growth in vehicle

parc is the key determinant of the future structure of the

world's auto industry. This growth and associated volume are

determined by sales and scrappage in individual countries,

depending on level of development in each country. North America

and Western Europe have been dominant players as measured by

their combined share of the world GDP. Vehicle density is the

number of vehicles in use per person in a country. In 1995 the

average vehicle density in the world was 117 vehicles per 1000 of

the world population. In the developed world, density was 547 per

1000 people, while in the developing world it was estimated as 34

per 1000. Thus vehicle parc equals density times population.

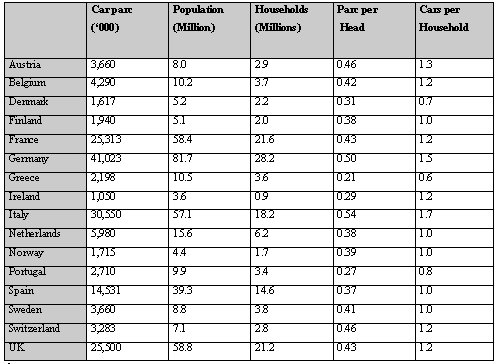

Table 3.4 above shows data on these terms for sixteen European

countries.

Thus the primary factors that drive the demand are population

size, vehicle density and average vehicle life. We expect vehicle

life to depend on GDP pr. capita and the price of cars in the

country in question, since wealthier populations tend to drive

larger cars. However we lack the empirical data to test this.

Vehicle density is determined by a number of factors. Undoubtedly

one of these is the price of vehicles. This price is often

distorted by a number of taxes on vehicles and on the use of

vehicles. Due to the variety of government imposed expenses on

vehicle use, it is not easy to get a clear picture of the tax

pressure in different countries.

Further there is reason to believe, that vehicle density is

related to GDP pr. capita, and to population density. These

relationships are examined in the two figures below. The figures

are made of data from table 3.4 and appendix B, by plotting GDP

pr capita and population density, against vehicle density.

Cars are regarded as a luxury good, and thus it is likely that

the vehicle density is highly affected by the wealth of a

country's population. This relationship is demonstrated in the

figure below. Here there seems to be a strong positive

relationship, between wealth and vehicle density.

Indsæt Figure 3.5 fra s. 34

Another hypothesis is that the level of car ownership is related to the population density of a country. The reason for this is, that in areas with high population density there is less need for long distance transportation, and public transportation is often more advanced in these areas. However as it appears from the figure below there seems to be no empirical evidence of this hypothesis. Quite surprisingly there seems to be a positive relationship between population- and vehicle density.

Indsæt Figure 3.6 fra s. 34

However, as it can be seen there is a very

large variation in the data. This implies that the tendency

towards a positive relationship between population- and vehicle

density is unlikely to be statistically significant. Thus we

cannot conclude that there is any relationship between the two in

Europe.

For both of the graphs there is the problem, that the data is

influenced by other factors, than the one measured (e.g. taxes).

This is especially a problem in this case, where we only have 16

observations, which is not enough to ensure that factors are not

biased towards a specific result.

Apart from the factors mentioned above, the demand for cars, like

all other products, is affected by substitutes and complementary

goods. As mentioned in section 3.1 the primary substitute for

passenger cars is public transportation. Consequently if public

transportation becomes more competitive through better service or

lower prices, demand for cars will be lowered.

Likewise if the prices of complementary goods are lowered, demand

for cars will increase. Among the most important complementary

goods are fuel and road taxes (In some countries). A less obvious

complementary good is finance. Cars are a major expenditure in

the budgets of most people, and thus they often need some sort of

external finance in order to purchase cars. Hence the interest

rate will affect the demand for cars. This relationship has

caused the largest car manufacturers to integrate into financing,

thus allowing more control of this factor. This is discussed in

section 3.3.4.

The effect of segmented markets

Below we shall discuss the causes, evidence and effects of

segmentation.

Under an agreement which came into force on January 1, 1993 the

European Union (EU) and the European Free Trade Association

(EFTA) have effectively merged to create the European Economic

Area (EEA), which extends many of the provisions of the post-

1992 single market to EFTA member states . This has been labelled

the world's largest integrated market.

However, the market is still highly segmented into national

markets. This segmentation is caused by a number of factors.

While economic integration may have created a market of 380

million consumers, those consumers have very different levels of

purchasing power. The disparities are demonstrated in table 3.2.

One of the central aims of the EU and the wider EEA is to reduce

disparities between regions through structural aid. The main

targets for structural aid are Ireland, Portugal, Spain and

Greece. On top of these economic inequalities there are

significant differences in climate topography, roads

infrastructure, population density and culture, which combine to

market diversity.

No matter what the reason, the fact is that the European market

at present is very segmented, even though there is a trend

towards increased integration of the European market.

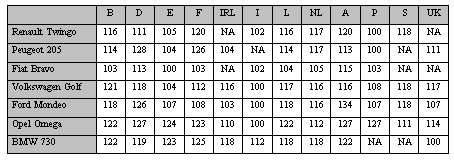

Table 3.5

Source: European Commission; Car prices

within the European Union on 1 November 1995.

Notification: B=Belgium; D=Denmark;

E=Spain; F=France; IRL=Ireland; I=Italy; L=Luxembourg

NL=Nethrlands; A=Austria; P=Portugal; S=Sweden; UK=United

Kingdom.

Evidence of this segmentation can be found in the prices of

cars across Europe. The table above shows prices of seven

different car models across Europe. Prices are calculated free of

tax as an index relative to the cheapest country. The figures are

from November 1, 1995. The brands selected for the table has been

chosen, in order to ensure maximum diversity across manufacturers

and segments. Thus we have chosen seven models from seven

manufacturers across six segments.

The table clearly shows that there are large differences in

prices across Europe. Further it shows that there are no clear

patterns with respect to cheap and expensive countries. In an

integrated market price differences should not exist, as higher

prices in one country would encourage the population to buy their

cars in other countries, thus levelling prices throughout Europe.

Since this is not happening, it must be because there are

barriers, and hence markets must be segmented.

The major effect of the segmented markets is that it allows firms

to price discriminate. In section 3.2.1 we discussed how a firm

facing a downwardsloping demand curve, will need to lower the

price on all units in order to sell an additional unit. In a

segmented market the firm can select a price in each market

independent from other markets. Thus if a manufacturer wishes to

sell an additional unit, he can do so by lowering the price of

all units in just that market.

A manufacturer that is able to price discriminate perfectly sets

a price on each car sold equal to the maximum the individual

customer is willing to pay (first degree price discrimination),

whereas a non-discriminating manufacturer will set the price at

the level the marginal customer is willing to pay. This can be

illustrated through the demand curve. The downwardsloping demand

curve indicates, that the first customers are willing to pay more

than the customers further to the right on the demand curve.

Consequently in a situation where there is only one price, some

customers are paying less, than what they would be willing to pay

if they had to. However a perfectly discriminating manufacturer

can extract this surplus for himself and thus earn higher

profits. This is demonstrated in the figure below.

Indsæt Figure 3.7 fra side 38

Segmented markets allow price discrimination on the basis of

national markets, and as it is shown in the figure this can be

used to get higher profits. However as it is also shown, the

benefit from discrimination depends on the slope of the demand

curve or rather the elasticity of demand. In infinitely elastic

markets consumers are willing to pay approximately the same

amount for different products, and thus there is no basis for

discrimination.

Since the slope of the demand curve faced by the individual

manufacturer depends on the level of industry competition as

argued in section 2.1, it depends on all the other issues

addressed in this chapter. For example a manufacturer in a highly

concentrated industry can more easily benefit from price

discrimination than a manufacturer in a more differentiated

industry, where competition sets limits for the prices the

manufacturer can charge. In the section summary we argue, that

competition in the industry is high, leading to rather elastic

demand. This decreases the gains from price discrimination.

Obviously no manufacturers in the car industry are able to

discriminate perfectly, that is on the background of the

individual consumer's willingness to pay. The car manufacturers

are merely able to discriminate on the basis of national markets,

and thus the size of the dark shaded area in figure 3.7 becomes

much smaller. The exact size depends on the shape of the demand

curve in the individual markets. Thus due to price discrimination

the manufacturers can set optimum prices in each market, which

yields higher profits than optimising from an aggregate point of

view. Consequently prices will be set higher in countries where

competition is weak and consumers are wealthy with elastic

demand.

The effect of segmented markets on competition can be discussed.

It is obvious, that segmented markets limit the extent of price

wars. If a price war occurs in one national market, this price

war does not automatically transfer to all other markets. Thus

the cost of price wars are lower in segmented market.

It can be argued that the lower cost of price wars increases the

likelihood of such wars occurring, thus increasing competition.

On the other hand segmented markets may also deter smaller

competitors from challenging larger firms. For example if a small

manufacturer enters the Dutch market, at a low price, the larger

competitors can relatively cheaply cut prices in that market in

order to outcompete the new entrant in a segmented Europe.

However in an integrated market, the large firm would have to cut

prices in all markets, thus making the move more expensive. Thus

competition from smaller competitors are limited in segmented

markets.

Market Power and Vertical Integration on the Demand

Side

The buyers of the automotive industry are a highly dispersed

group. Most of the cars produced end up in private ownership,

even though a few are sold to rental or leasing companies. Also

many companies provide cars for employees that need the vehicle

in their daily work.

Most cars are sold through dealerships, which are in most cases

not owned by a manufacturer, even though they often have strong

relations to specific manufacturers . The investments made by

these dealerships are quite small, since they are not required to

do any R&D or investment in any specialised assets. Hence if

dealers are dissatisfied with the manufacturer, or the other way

around, they can quite easily swap to another. Thus there exist

little buyer power in the relationship between the manufacturers

and dealerships.

Due to this low market power, transactions are often done at

arms-length, and there is little need for vertical integration

into dealerships .

However in some ways the manufacturers have invested into

distribution. Thus all of the seven largest manufacturers

described in chapter 5 have established financing companies .

These companies provide finance for the individual buyers, as

well as the dealerships, which need to finance their stock of

vehicles.

The financing part is very important in the decision whether to

buy a car, and in most instances the cost of financing is part of

the total cost of the car. Thus owning financing companies, allow

the manufacturers more control over the cost of the cars. Also

car manufacturers are usually, as mentioned in the introduction

very large companies with deep pockets, and thus they are able to

provide this finance.

Another important feature of the integration of financing

companies is that it is an alternative to vertical integration

into dealerships. Since the owners of these dealerships usually

do not have the funds to invest in a stock of cars and parts some

sort of financing is needed. The financing companies of the large

manufacturers provide this finance. Without these vertical

integration into dealerships might be necessary.

Further some of the companies have invested in car rental

companies. An example is Ford that bought Hertz in 1987 . This

action can hardly be explained from a market power approach, but

rather that Ford wished to ensure a secure demand for their

vehicles, while entering a profitable business.

SUPPLIERS

It is not the intent of this report to conduct a thorough

analysis of the car components industry. Instead we will merely

point out the special relationship between component

manufacturers and assembly companies.

For this we shall use the theory of transaction costs, as a

determinant of vertical integration. We shall also point out the

relationship between market power and vertical integration.

Further we shall briefly discuss the barriers to forward

integration by component manufacturers, and the importance of

good supplier relations to competitiveness.

Market Power and Vertical Integration

Market power exists when one side of a relationship is more

dependent on the other, than the other way around. E.g. A is more

dependent on B, than B is on A.

Market power often occurs as a consequence of transaction costs.

In the car industry transaction costs occur due to asset

specificity. Often component suppliers are required to invest in

very specific assets, in order to produce the components for a

specific manufacturer . This specificity of assets lead to the

possibility of opportunistic behaviour by the manufacturers, as

they face the opportunity of demanding lower prices after the

specific investment has been made.

The reaction of component producers is to secure themselves

against this risk. This can be done through charging a premium or

demanding a long-term contract. In both cases there are

transaction costs, as the long-term contract doesn't allow for

flexibility in either price or product, as the industry changes

over time.

Thus the required investment in specific assets lead to market

power, since manufacturers may act opportunistically. This leads

to transaction costs, as component producers seek to protect

themselves from opportunistic behaviour. One way to eliminate the

chance of such behaviour is vertical integration since it removes

the incentive for opportunistic behaviour.

Consequently vertical integration in the car industry is much

more likely on the supply side than on the demand side.

Manufacturers are especially likely to integrate vertically into

components that are specific for the single manufacturer, and

require large investment in assets. In chapter 7 we have tried to

quantify the level of vertical integration for 4 manufacturers.

An alternative to vertical integration, is close co-operation

with component manufacturers, which is an integral part of the

Japanese Just in time system. We will not discuss this phenomenon

any further.

Barriers to Forward Integration

In the case where the component manufacturers have the

opportunity to integrate forward into assembly of cars this would

increase competition. However, all of the component producers

face the same barriers as everyone else. These include economies

of scale, R&D and branding.

Further if component producers attempt forward integration, they

will do so at the risk of loosing existing revenue, as assembly

manufacturers are unlikely to help a potential competitor.

The Importance of Supplier Relations

Supplier relations are very important to car manufacturers, as

they are needed in the car aftermarket.

As a consequence of vertical integration, car manufacturers make

some of their own components. The production of these components

is under the control of the manufacturer. However production of

components sourced from other firms may pose a problem in the

aftermarket. The aftermarket is the market for components and

service after the initial sale of the automobile. Problems may

arise if these suppliers choose to discontinue production of

parts that are used in vehicles no longer in production. Since

these vehicles are still in use, there is still a small demand

for such parts, in the case of repairs. Often this demand is too

small to sustain production of these parts, however they are

essential to the manufacturer, because the price and availability

of aftermarket sales and services of older models affect the sale

of new models . Thus car manufacturers are dependent on their

relationship to component suppliers, with respect to the

availability of parts for repair. This is a further reason for

vertical integration.

BARRIERS TO ENTRY

Barriers to entry are highly important to the profitability and

competition of an industry, since low barriers to entry will

encourage new entrants in the industry, until economic profits no

longer exist. Thus competition is lowered through high barriers

to entry. Below we shall discuss the barriers that are relevant

to the car industry.

Economies of Scale

Economies of scale are often cited as a factor leading to entry

barriers. In industries where economies of scale are significant,

firms need a large volume of production in order to stay in the

industry. If a company does not have such volume, it will face

higher average costs, than other firms, and will eventually

perish under the forces of competition from larger market actors.

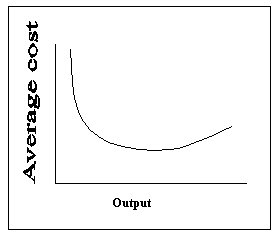

Economies of scale occur when companies face a downwardsloping

average cost curve. However as it is indicated in figure 3.8

below, average cost usually only drops for a while, before it

flattens and eventually starts to rise.

Figure 3.8

Economies of scale work as an entry barrier, because firms who

wish to enter the industry, must have enough volume to produce at

the flat part of the slope. The minimum required volume is called

the minimum efficiency scale (MES).

One type of economies of scale arises as a consequence of fixed

costs. Often if production is large enough, it is profitable to

invest in a more efficient production plant, which lowers the

marginal costs, but increases the fixed costs.

Scherer and Ross suggest that minimum efficiency scale for a car

production plant is 200.000 units . Obviously this is a very

rough estimate, since it doesn't take into account that different

car models are likely to require different production plants.

However, minimum efficiency scale is very difficult to estimate

accurately, but 200.000 units are not very much taking into

account, that Ford alone produced 7 million cars in 1997

worldwide . Further evidence against product economies of scale

as an entry barrier can be found in the fact that most

manufacturers operate more than one plant. Thus it appears that

economies of scale is only an entry barrier for the smallest and

often specialised companies. Hence economies of scale might be an

argument for producing a wide range of vehicles in different

segments, since many of the factory operations are the same, no

matter which model is being made.

For larger companies there are no product economies of scale,

since these manufacturers far exceed the minimum efficiency scale

of 200.000 units. However there is still theoretical evidence

that there are economies of scale for large manufacturers, which

will be discussed in chapter 8. These economies of scale are

likely to relate to fixed and sunk costs, which do not relate to

quantity of output. Here we think especially of R&D, but also

of marketing.

R&D will be discussed separately below, and quantified in

chapter 7.

Research and Development

On average the five manufacturers Ford, GM and Volkswagen spent

5,8% of sales (weighted avg.) on R&D (See Section 7.4 for

details). This is way above the average industry, which spends

approximately 0,8% of sales on R&D . For comparison the

average in ethical drugs is 10,2% and in semiconductors 6,1%.

Although an industry average for the car industry has not been

available, it appears that the car industry is very intense on

R&D. The reason for this can be found in the special

industrial structure. Throughout this chapter we have discussed

factors that limit and facilitate competition. In the section

summary below it becomes clear that the car industry is basically

highly competitive, but at the same time there are factors that

contribute to a bit of market power for the individual firm.

This is a structure that is ideal for facilitating R&D

spending. In a situation of perfect competition where the

individual firm faces a perfectly elastic demand, there is no

incentive for companies to spend money on R&D, since all

firms will earn the same profits. However in such a situation a

revolutionary innovation, might help to change the market

structure. On the other hand in a situation, where the individual

firms have large market power, and face little competition, there

is little incentive for innovation and R&D . This thesis is

based on a Schumpeterian argument, where disruption and threat is

a catalyst of innovation. Such disruptions are small in

established monopolies.

Another interesting aspect of the average percentage of R&D

for the companies above is that it is above the industry average.

Since these companies are among the largest in the industry, it

seems that R&D is necessary for growth and success in the

industry. This gives R&D a role as an entry barrier, since

most small companies cannot afford the large expenditures

connected with R&D. At the same time R&D costs are sunk.

Thus there are significant economies of scale connected to

R&D, which further facilitates its role as a barrier to

entry.

Brand Identity

Brand identity is closely related to marketing expenditure. For

Ford and General Motors this equals approximately 2,4% of sales

revenue. In 1977 the average industry spend 0,66% of revenue on

advertising , but this figure has probably risen as a consequence

of the increased public attention towards mass media. Thus the

car industry appears to have marketing expenditures close to the

average industry.

However Brand identity may still work as a powerful deterrent to

new entrants. The purchase of a car is a major expense for most

potential customers. Therefore it is important for the customer

to be certain, that he is buying a quality product, and that he

can acquire spare parts and service should a problem arise.

Consequently it is important for manufacturers to have a strong

public profile of stability and quality. Well-established

companies can provide this more easily than newcomers.

Due to the combination of high price and a wide variety of

manufacturers and product lines, potential buyers are likely to

involve themselves in the purchase. Hence it becomes important

for the manufacturers to provide information about their products

to their customers. This further increases the importance of

marketing.

Product differences

R&D and marketing both contribute to product differences in

the car industry. R&D because it allows the manufacturers to

develop new and different models, marketing because it gives

consumers different perceptions of the manufacturers in the

industry.

Thus the internal substitutability in the automotive industry

becomes imperfect. This means that consumers are not indifferent

to which car they purchase. Further it means that the car market

becomes less transparent, and thus it is difficult for the

consumers to evaluate how to get most value for their money.

In a situation of imperfect substitutability each manufacturer

faces a slightly downwardsloping demand curve, or rather the

manufacturers have some power over prices. As mentioned in

section 3.2.1 a downwardsloping demand curve indicates some

market power and thus some monopoly rents. Consequently product

development and marketing lead to product differences, which

again lead to market power. This market power decreases the level

of competition somewhat, and keeps the industry away from a

situation of almost perfect competition.

Government Policy

Several important aspects of automotive design are subject to

government regulatory standards. While regulatory standards are

primarily aimed at achieving two common social objectives,

vehicle safety and environmental protection, they differ greatly

from one market to another. Nations and regions independently

have developed their own automotive regulatory standards with

accompanying certification and testing procedures over time. As

the automobile marketplace has become increasingly global,

differing regulatory standards have become a major barrier to

trade. Thus these regulatory differences are highly important in

segmenting the European market (See section 3.3.3).

Compliance with multiple regulatory frameworks reduces vehicle

affordability as it imposes substantial cost penalties and design

manufacturing constraints. It is fundamentally inconsistent with

free trade in a global automobile market. It also extends the

time needed to develop new products, preventing manufacturers

from responding quickly to the changing needs of consumers'

world-wide. As it will be argued in the next chapter, exactly the

quick response is an important source of competitiveness.

Additional costs incurred to design and develop different

versions of a particular model simply to meet different

regulatory and certification requirements may add more than 10

percent to the design and development cost of the product. Higher

costs mean higher prices for consumers and reduced choice of

products

There are two mechanisms by which government intervention is

contributing to the emerging shape of the automotive industry:

environmental regulation and co-founded R&D programs.

With regard to environmental issues, certain town and city

centers have been closed to traffic, and incentive schemes have

been set up. Among these are cars fitted with catalytic

converters, scrappage incentives, and electric vehicles .

With regard to R&D it is essential that public authorities

support the research and development efforts of the industry. EU

has a key role in stimulating joint research and technological

level between companies within the industry as well as on a wider

multisectoral basis. It is to Europe that credit must be given

for the major advances of recent years (injection, ABS, power

assisted steering automatic gearbox, converter, etc.).

Europe's technological capability in the automotive sector is

great. But in the field of research and development going beyond

basic research, European co-operation in global terms is lagging

behind the United States and Japan .

State aids remain a controversial area of the EUs competition

policy. The actual orientation of governments is for the reform

of state aid control and for more transparency in the

Commission's decision-making process for the approval of state

aids granted by Community governments to public and privately

owned enterprises.

State aid weakens the competitiveness of the European industry.

First it can lead to distortions within the market, which lead to

inappropriate levels of outputs and perhaps inefficiency.

Secondly, it can distort the nature of the oligopoly game,

leading to unfair advantages or if governments engage in matching

each other in the aid given to their own national firms socially

wasteful expenditure .

The reason for using state aid in the car industry, is that it

employs a lot of people, contributes a lot to a country's Gross

Domestic Product and car makers want to sell cars and will invest

behind barriers to do so.

All in all government policy has large effects on competition.

The different standards in the different countries help to

segment the market, making price discrimination easier, while

state aid works as an entry barrier to keep out new potential

entrants

SECTION SUMMARY

In this section we have used Porters framework to evaluate

different features of the industry, with respect to their effect

on the level of competition. Further we have established some

relationships between these features and the conduct of market

actors.

Substitutes were used to define the industry as the companies

that assemble motorised vehicles for personal use. We further

argued that the closest substitute is public transportation, but

that this poses no real threat to the industry at present.

Further we have shown that the European car industry is

characterised by a moderate concentration, which allows the

manufacturers little market power. There is a large amount of

overcapacity in the industry, which induces heavy competition. In

spite of this manufacturers are still investing in production

plants, which we suggest is a consequence of game theory and

strategic thinking. Although the sunk costs are relatively high

in the industry, this doesn't lead to high exit barriers, because

production assets are industry rather than firm specific. Thus

the companies are able to sell their assets at a reasonable

price. The markets for cars in Western Europe are saturated, and

thus industry growth is rather small, which leads to tough

competition for the existing customers. The fixed costs of the

industry are, however, an incentive to cut costs.

Germany dominates the demand in the car industry, followed by

France, Italy, UK and Spain. The main factor driving demand is

economic prosperity. The buyers of cars are highly dispersed, and

thus have little power. The segmentation of the European market

has allowed the use of price discrimination, which increases

profits.

Due to specialised assets there are a larger potential for

vertical integration on the supply side of the industry. Car

manufacturers are somewhat dependent on their suppliers for

components for vehicles that are no longer in production.

The main barrier to entry is the high costs of R&D, followed

by the importance of a good reputation. Economies of scale in

production do exist, but with a minimum efficiency scale of

approximately 200.000 units, it only affects smaller

corporations.

R&D and brand identity both contribute to product

differences, which allows the manufacturers a little market

power.

Of the factors mentioned above, the following facilitate a high

level of competition:

# Overcapacity

# Low industry growth

# Supplier dependency

# High fixed costs

The following factors limit the level of competition:

# No close substitutes

# Moderate Concentration

# Insignificant exit barriers

# Dispersed buyers

# Entry barriers due to R&D costs

# Product differences.

In spite of these factors the car industry is highly competitive.

The reason for this is that the factors that limit competition

only provide marginal market power. For example the concentration

and product differences that are large enough to provide

manufacturers with a little discretion over prices, and a

slightly declining demand curve, but too small to provide any

real monopoly power.

The factors that facilitate competition on the other hand are

very powerful. Especially the overcapacity has led to a very

competitive environment, as all manufacturers try to increase

their sales through lower prices in order to use their capacity.

Thus all in all we will characterise the European Automotive

industry as highly competitive.