The European Automotive Industry

FUTURE OF THE INDUSTRY

In this chapter we shall discuss how some of the factors

discussed earlier in the report are likely to change, and how

that will affect the car industry.

ECONOMIES OF SCALE

Over the past decade there has been a trend towards increased

concentration in the car industry. This has been demonstrated

through a number of mergers in the industry, the latest being

Chrysler and Mercedes-Benz. So far there is no indication that

merger acti-vity will cease in the near future. It can be argued

that for each of these mergers, there is a distinct reason, and

thus that this is not a general trend. For example, the above

Chrysler-Mercedes merger is related to market access, while it

can be argued, that the Rolls Royce BMW deal is related to

prestige and thus marketing.

In spite of this we think that the merger activity is a general

trend towards a new equili-brium with fewer firms in the

industry. The cause of this is discussed through the theore-tical

argument below.

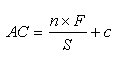

The theory is based on the argument, that in a competitive

industry price must equal ave-rage costs, as positive economic

profits would lead to entry, whereas negative economic profits

would lead to exit. The average cost function can be described by

the equation below:

Where: n = number of firms; F = Fixed costs; S= Size of

industry;

c = Variable costs.

The argument is that AC includes variable costs and a share of

the fixed costs. Fixed costs must be incurred by all the firms in

the industry, and thus the more firms in an industry, the higher

the average costs.

The price function in the industry can be described by:

![]() Where b is a

constant; n = number of firms; c = variable costs.

Where b is a

constant; n = number of firms; c = variable costs.

Hence price equals variable costs + a margin that decreases with

the number of firms.

Thus price decreases with an increased number of firms, while

average costs increases. In equilibrium price equals average

costs. This is demonstrated in the figure below.

Indsæt figure 8.1

fra side 94

Source: Krugman and Obstfeld; page

130

As it appears in the figure a decrease in the number of firms

can happen either through upward move by the AC curve or a

downward move by the P curve. Referring to the two equations

above, this can happen in case of increased fixed costs, or

decreased variable costs.

An immediate impulse is that the merger activity in the car

industry happens as an effect of decreased variable costs, due to

better production technology. It is likely that produc-tion

technology has decreased variable costs in the industry, but that

does not explain the ongoing concentration, since c appears on

both sides of the equation P=AC. Thus the im-proved production

technology simply lowers the cost and price of products, but

doesn't change the equilibrium number of firms in the industry.

Hence the only explanation for the merger activity is increased

fixed costs.

As we have discussed earlier in chapter 3 such fixed costs are

likely to relate especially to R&D. Thus it appears, that the

increasing R&D costs, and the need for constant introduc-tion

of new models are causing a concentration in the industry. This

allows firms to use their R&D across several models.

Another issue relating to economies of scale is minimum

efficiency scale. It has been argued that new production

technology is leading to lower MES . Theoretically this should

allow for a deconcentration in the industry, as smaller players

can operate at an efficient level. However as mentioned above the

trend goes in the other direction, with increased concentration.

The reason for this contradiction is, as already discussed in

section 3.5.1, that an MES of 200.000 units is so small, that it

only affects smaller market actors. In other words the economies

of scale in production are much smaller than eco-nomies of scale

in R&D. Hence MES is not very important among the large

players in the automotive industry.

CONCENTRATION AND R&D

As discussed above the industry is likely to experience

concentration as an effect of in-creasing R&D costs. The

question is whether this will decrease the level of competition

in the industry.

With an HHI of 1012, the concentration is not very high at

present. Thus even if concen-tration increases a little, this is

not likely to decrease competition. One reason for this is the

large overcapacity in the industry, which will force market

actors towards 7intense competition.

Another reason for a likely concentration increase, is the

ongoing globalisation. This makes it necessary for manufacturers

to be present in all major world markets, in order to stay

competitive. Smaller firms do not have the resources to compete

in all major mar-kets, which leads to further pressure for

alliances or mergers.

VERTICAL INTEGRATION

Car production is increasingly specialised. Hence manufacturers

need increasingly speci-fic components. This makes substitution

on the supply side more difficult, which increa-ses the market

power tension, thus making vertical integration more likely, as

described in section 3.4.1. A prerequisite for the rise of such

market power is that the specialised components require

specialised assets.

However, it can also be argued, that new management thinking is

leading in the other direction. The success of Japanese

manufacturers, with their system of very close tran-sactions in a

non-integrated environment, has spurred European and American

producers to seek opportunities in the same direction. Thus this

new thinking poses a threat to the conventional idea of

integration versus arms-length transactions.

Another reason for less vertical integration is differences in

MES. As mentioned above in section 8.1, MES is decreasing in the

car industry. This automatically leads to higher dif-ferences in

MES for the manufacturing and car component industry. For example

if MES for manufacturing drops to 175.000 units pr. year, while

MES for a specific component is 400.000 units, integration is

less likely to happen.

All in all it is not possible theoretically to argue how vertical

integration is likely to change in the future. However it does

appear that there is a trend towards lower value added within the

car industry. For example in the analysis conducted by Karel

Williams of this phenomenon for the period of 1980 to 1991 there

are indications of much higher levels of vertical integration for

PSA and BMW than our analysis indicates. However the methodology

of these analyses are quite different, making comparisons

difficult. Volks-wagen is the only company that provides data on

material costs for an extended period of time. These data show

that material cost as a percentage of costs of sales increased

from 64% in 1988 to 67,5% in 1997 indicating a slight decrease in

vertical integration .

SEGMENTED MARKETS AND INDUSTRIAL POLICY

As we have discussed in section 3.3.4, the national markets in

Europe are heavily seg-mented. This segmentation has occurred,

due to a number of differences. A very impor-tant one among

these, are differences in regulatory environments.

However with the trend towards continued European Integration,

some of these differen-ces are likely to converge over time.

Hence markets will become less segmented, and thus manufacturers

will loose the opportunity of price discrimination. This will

definitely lead to lower profits in the industry. The effect on

competition is more difficult to estimate. As we have argued in

section 3.3.4 the effect of price discrimination on competition,

is not clear, and thus we will have to wait and see.

For the world as a whole the tendency is in the exact opposite

direction. With the rapid development of new markets in

developing countries, there is a high risk that the number of new

regulatory requirements world wide will escalate quickly,

creating new technical barriers to trade. As mentioned several

times throughout this report, we focus on the European industry

only. However this global trend towards different regulations,

will also affect the actors that concentrate on the European

market. The reason is that the costs of testing and adapting car

models for different regulatory environments, is a sunk cost, and

thus much of the savings in the European Market, will be absorbed

by regulations in other markets. Thus testing and adaptation

costs cannot be expected to fall in the near future.

All in all it can be said, that government regulation has two

opposite effects on profit-ability. On one hand it allows price

discrimination, while on the other it increases costs of testing.

Another issue with respect to government interference, is the

increased focus on en-vironmental transportation. More and more

regulations and incentives for this purpose are being introduced.

This will cause manufacturers to focus more on smaller vehicles.

This is not really an industry structure issue, but rather a

marketing issue. However, it might have severe effects for

companies at the high end of the market. These companies will be

forced to move into lower segments, thus increasing competition

in these segments.

The last issue under government policy is that in the future, EU

regulations will make any kind of government subsidies difficult

to implement. This of course removes a barrier to competition.

OVERCAPACITY

As discussed in section 3.2.2 there is presently overcapacity in

the industry. Since most of the actors are contemplating new

investments, there seems to be no reason for this situa-tion to

change. Further as argued in section 3.2.4, there is no reason to

believe, that a growth in demand will cancel the effects of

overcapacity. This overcapacity is a very strong argument for

continued heavy competition in the industry, which will lead to

fur-ther restructuring.

ARENAS OF COMPETITION

With respect to the arenas of competition, we do not expect

significant changes, over the next years.

It has been argued that uniform regulation in the EU and

pressures for smaller cars, will lead to a commoditisation of the

car market . This would lead to more elastic demand, and thus a

higher level of competition. In such an environment, there would

be no possi-bility of escaping the price pressures through

differentiation, putting even more emphasis on the cost

efficiency.

However there are also arguments in the opposite direction. As we

argued in section 8.2, there is a tendency towards lower MES in

the industry. This will make diversity among models more viable,

as it will no longer be necessary to produce similar cars in

order to use the same production plants. Eventually this would

lead to increased differentiation in the industry.

In the timing and know-how arena, efficient R&D will uphold

its importance, in an incre-asingly competitive environment,

where companies are required to improve constantly in order to

survive. This is in line with D'Avenis theory suggesting that in

all industries competition increase over time.

As we have already mentioned in section 4.5, deep pockets are of

great importance in a restructuring industry. As a consequence of

the overcapacity, this restructuring is likely to continue. Thus

deep pockets will remain an important advantage.

SECTION SUMMARY

In this chapter we have argued that a restructuring is currently

in process and that this is likely to continue. Thus we expect

continued mergers in the industry. Further we have argued

theoretically, that the reason for this is increased fixed costs,

most likely con-nected to increasing R&D expenditures.

Mergers will lead to an increased concentration as measured by

the HHI. However, it is unlikely that this increased

concentration will lead to increased market power and de-creased

competition, since the HHI is still relatively low, due to the

large number of equal sized competitors. Further, the

overcapacity is likely to continue in its role as a powerful

catalyst of competition.

It can be argued that vertical integration on the supply side is

likely to increase as a con-sequence of increased need for

specialised components and assets in the component indu-stry.

However, the trend is in the other direction, which is likely to

be a consequence of new management thinking and MES

differentials.

The segmentation of European markets is decreasing, because of

the increased integrati-on. This is especially important with

respect to harmonisation of technical standards. The effect of

the integration, is that manufacturers will loose the opportunity

to price discri-minate, but will be able to cut costs on testing

and adapting models for different markets. Further the increased

focus on environmental issues, will push the manufacturers

towards smaller cars. This will lead to increased competition in

the C and D segments.

Finally we have argued, that competitiveness is likely to be

based on the same factors in the future, namely low cost

production and efficient R&D. Also financial resources are

important, while the industry is restructuring.